The mobile gaming market closed 2025 with numbers that are hard to ignore. The App Store generated $90.6B in total revenue — up from $62.3B in 2024. Google Play added $52.3B. The combined market across both stores reached ~$143B, with games holding a significant share: 53.9% of Google Play revenue and 46.7% of App Store revenue.

But the structure of the mobile gaming market has shifted. Non-gaming apps — AI subscriptions, streaming, lifestyle tools — started closing the revenue gap for real. Downloads on Google Play held steady at 108.9B, while the App Store grew to 47.4B. UA costs went up, organic traffic got harder to capture, and the window for launching an average app and hoping for the best closed for good.

The winners of 2025 weren't the fastest to ship. They knew their unit economics before launch, not after. In this article — our data from the Mobile App Market Report 2025, three strategies that worked, and mobile gaming market trends for 2026.

iOS vs Android: Two Different Business Models

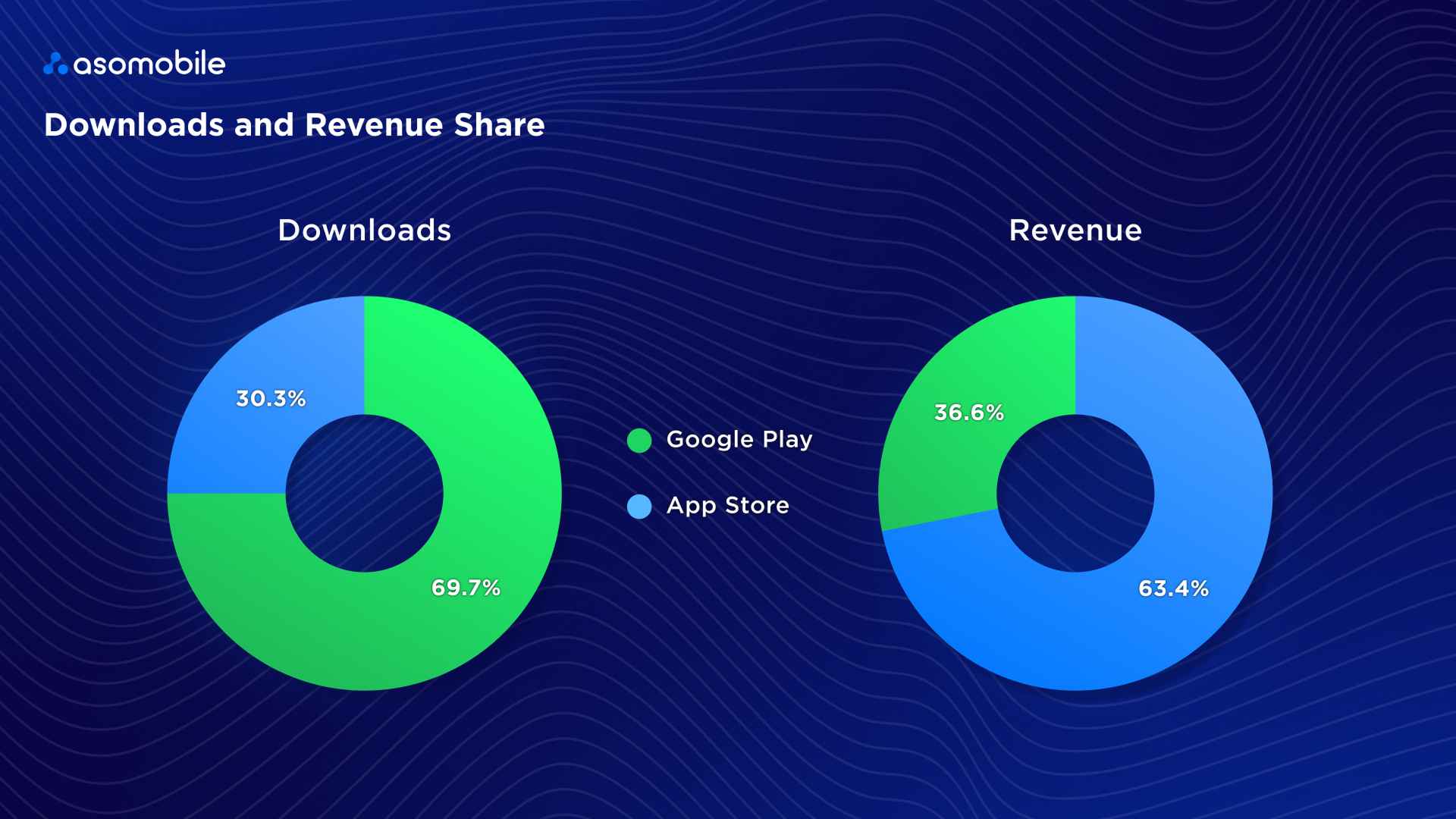

The platforms don't just differ in audience size. According to our data, the App Store accounts for 63.4% of combined revenue but only 30.3% of downloads. Google Play drives 69.7% of installs but generates just 36.6% of revenue.

| Metrics | App Store | Google Play |

| Revenue share | 63.4% | 36.6% |

| Download share | 30.3% | 69.7% |

| Primary model | Subscriptions + IAP | Ad-driven (IAA) |

| Day-1 retention | ~28–35% | ~25–32% |

Google Play is where we stress-test our servers and validate mechanics with a real audience. The App Store is where we build a sustainable business model. Both matter — just for different reasons.

One thing worth keeping in mind when planning: downloads and revenue in games barely correlate. Casual games dominate installs through broad appeal and a low barrier to entry. Revenue concentrates in midcore and strategy games with deep economies and long player lifecycles. These are two different product strategies — and confusing them is expensive.

Three Games, Three Completely Different Playbooks

The download slump didn't stop three titles from breaking through in 2025. Each did it differently — and these strategies directly contradict each other.

Block Blast! — zero IAP, and it worked

Block Blast! topped download charts on both stores combined, beating Roblox. Hungry Studio launched with zero in-app purchases in a market saturated with aggressive paywalls. Pure gameplay, 100% ad monetization, offline support. According to our data, Block Blast consistently held a top-5 position by downloads on Google Play from October through December 2025 — appearing in the charts seemingly out of nowhere in the second half of the year.

The loop retained players so well that spending incentives weren't needed — they just kept coming back. If our game's core loop works, IAA monetization can still take us to the top of the charts.

Last War: Survival — a genre bait-and-switch that turned out to be honest

Those ads with the little soldier running through multiplier gates aren't fake. That's the actual onboarding. Last War used a casual arcade hook to acquire players cheaply (low CPI), then gradually transitioned them into a deep 4X strategy game with high LTV. According to our data, Last War: Survival consistently held a top-3 revenue position on the App Store for most of 2025.

Mixing genres in our project isn't risky if the funnel is intentionally designed.

Pokémon TCG Pocket — selling the feeling, not the gameplay

The team spent their budget on the sound of a foil pack tearing open, the haptic feedback when a card slides out, and the holographic sheen on a rare pull. It captured collectors, not just gamers. The result: a consistent top-5 revenue position on the App Store in key markets including Japan and France.

In 2025, sound design and haptics in our game aren't final polish. They're retention tools.

Why the Same Games Keep Winning

The revenue top 10 barely moved in 2025. That's not inertia — those are repeatable mechanics worth studying before we design our own monetization.

| Game | Why it holds | 2025 revenue | 2025 downloads |

| Honor of Kings | Social infrastructure in China, 98% domestic revenue | ~$1.68B | ~45M |

| Roblox | User-generated content, primary social network for Gen Alpha | ~$1.45B | ~295M |

| Whiteout Survival | 4X mechanics wrapped in a survival theme accessible to a wide audience | ~$1.40B | ~58M |

| Royal Match | No ads — players pay for boosters to stay in the flow | ~$1.37B | Not in top 10 |

| Free Fire | Optimized for low-end devices, dominant in Latam, India, Southeast Asia | ~$366M (iOS) | ~287M |

Royal Match deserves a closer look: not in the top 10 by downloads, but generating over a billion dollars a year with no advertising inside the game. The entire model is built on players choosing to pay to keep playing. If we're designing monetization, this is worth studying in detail.

Which Genres Are Growing

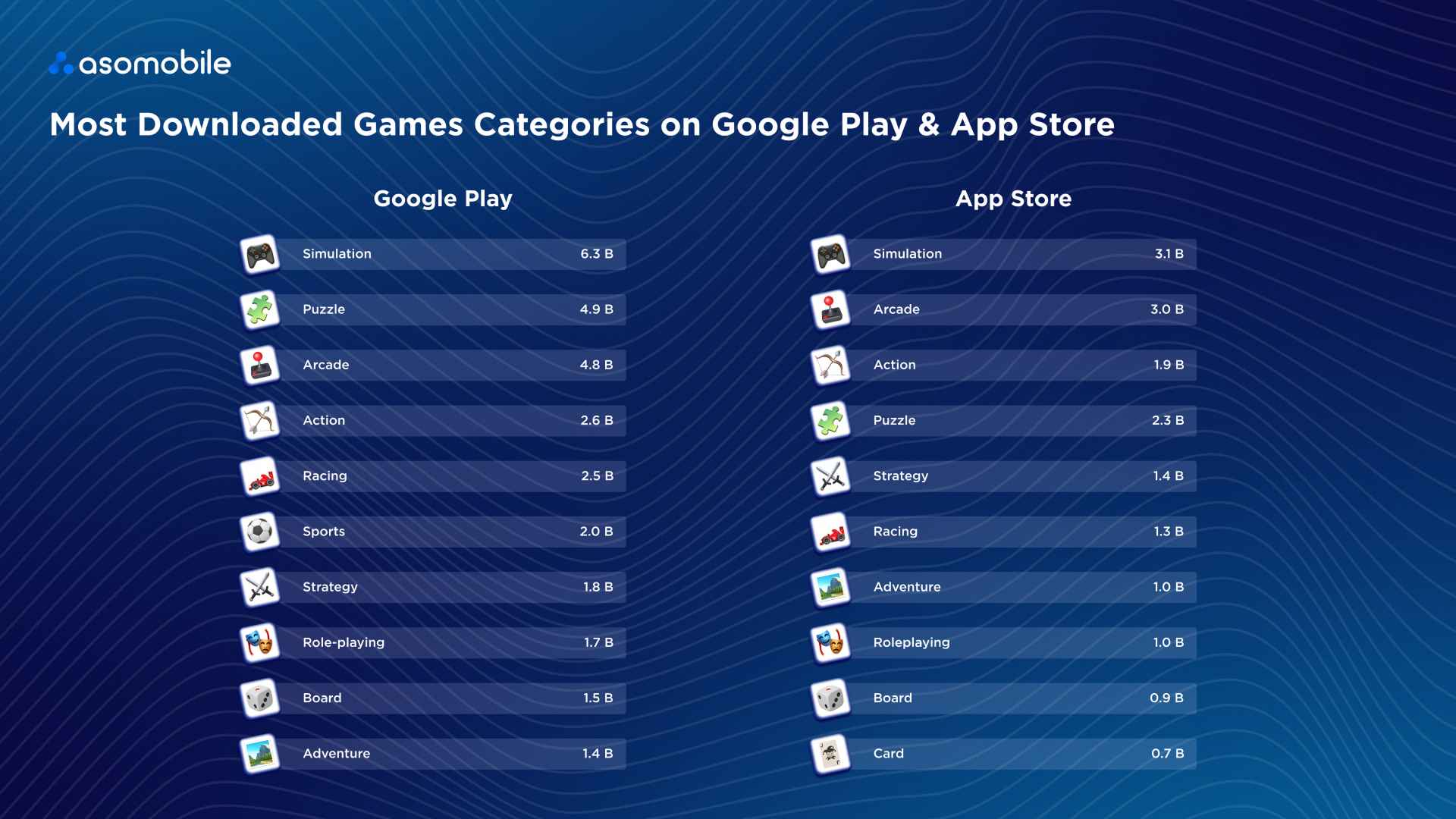

By downloads, Simulation leads on both stores — 6.3B on Google Play and 3.1B on the App Store. Puzzle and Arcade follow. These genres attract a mass audience through a low barrier to entry.

By revenue, the picture is different. On Google Play, Strategy ($6.6B) and Roleplaying ($6.1B) lead. On the App Store — Roleplaying ($9.1B) and Strategy ($8.3B). Midcore and hardcore convert audiences into revenue more effectively than casual — they just work with a different type of player.

The practical takeaway: if our goal is install volume, we look toward Simulation and Arcade. If our goal is revenue, Strategy and RPG with deep economies deliver a different result.

Mobile Gaming Market Trends for 2026

Sessions are getting shorter

Our games compete with TikTok for the same 90 free seconds. Long tutorials and slow ramp-ups don't survive in that context. Block Blast proved it: no tutorial, instant loop, works offline. If our game doesn't deliver a reward within 90 seconds, the player leaves before they've had a chance to like it.

AI is changing creative production, not creative direction

A single ad creative degrades after roughly four exposures to the same user. Producing variations manually is too slow and too expensive. Studios that use AI to generate and test hundreds of variants — not to replace creative judgment, but to consistently feed the algorithm — run lower CPIs than those still building ads one at a time. Speed has become a structural advantage here.

Algorithms need signal volume

Meta and Google's ad algorithms need roughly 50 conversions per week to exit the learning phase and start optimizing effectively. If our budget is spread across eight networks, none of them gets enough data. We concentrate our spending on two or three channels, let them learn, then expand. A fragmented budget produces fragmented results.

Incrementality testing is no longer optional

Standard attribution overstates paid performance by crediting organic users to paid channels. Incrementality testing — running a holdout group with ads turned off — shows how many installs our campaign actually drove versus how many would have come anyway. Without it, we're optimizing based on numbers that don't reflect reality.

Web shops have become the standard

More than 72% of top-grossing games now operate external web stores. Apple takes 30%, and payment processing on our own site costs roughly 5%. We can pass some of that margin back to players as bonus currency for purchases made on the website. Tools like Xsolla and AppCharge have made this viable for mid-sized teams. If we have a Discord community, we already have the foundation for a direct monetization channel.

Where to Launch in 2026

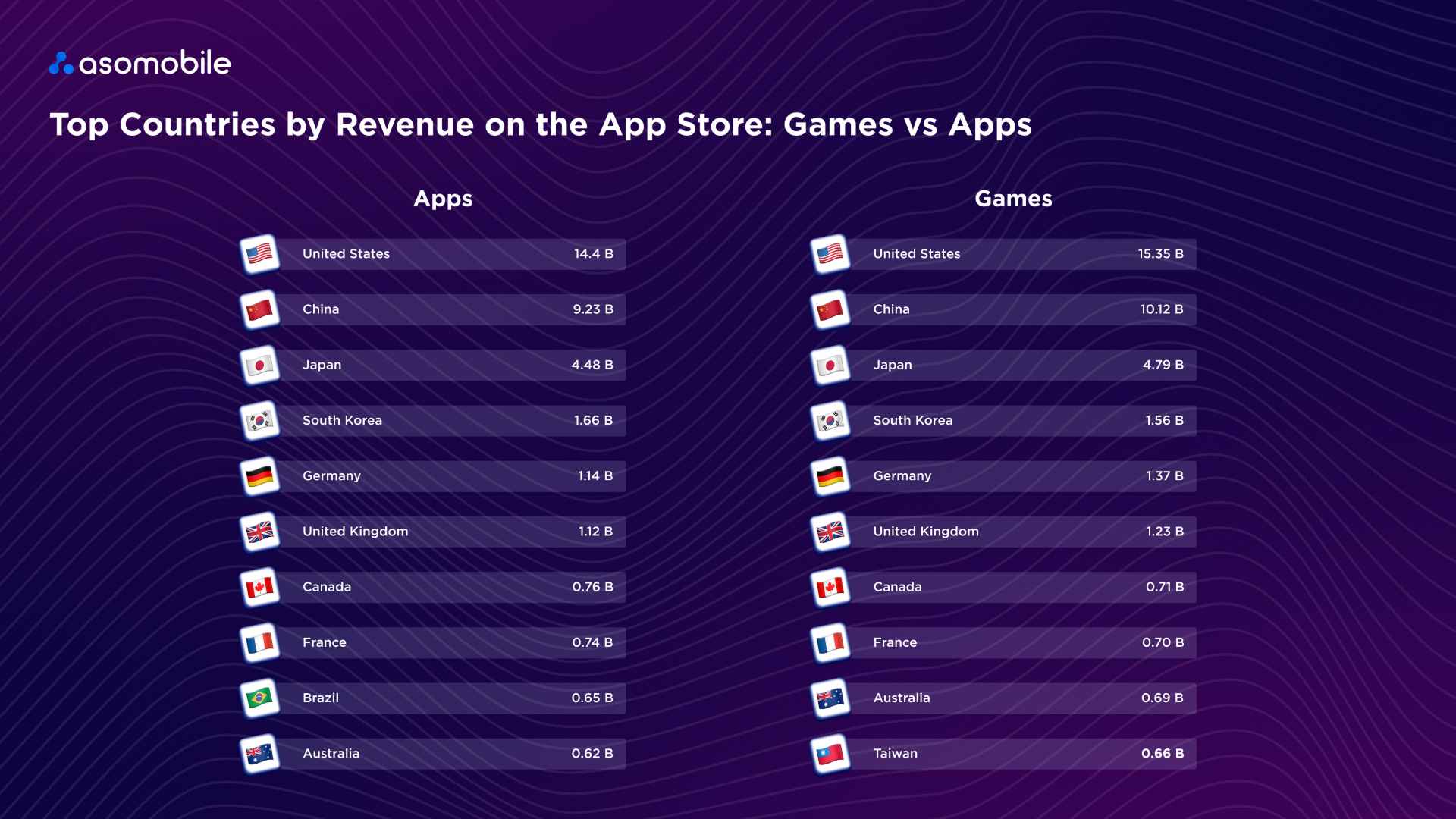

United States — $15.35B in game revenue on the App Store alone. The largest market by revenue, but growth is flat, and competition is expensive. Entering without strong ASO and proven unit economics means burning through budget fast.

Japan — $4.79B in game revenue on the App Store. The highest ARPU in the world. Gacha mechanics and strong IP convert here better than anywhere else. Last War and Pokémon TCG Pocket consistently held top-5 revenue positions in the Japanese market — not by accident.

South Korea — $1.56B in game revenue on the App Store. A market that punches significantly above its demographic weight and responds well to deep RPGs and strategy games.

China — $10.12B in game revenue on the App Store, $2.56B on Google Play. A closed market with specific entry requirements, but Honor of Kings clearly shows what the ceiling looks like with the right product.

Brazil and India — volume markets. Google Play saw 8.25B game downloads from India and 3.11B from Brazil. ARPU is low, but if our model is ad-based, presence here is non-negotiable.

Turkey — the testing market. Low CPI, revenue growth of +28% in 2025, and a mature developer ecosystem. Royal Match grew here — that's not a coincidence.

Our 2026 Forecast

Competition is shifting from traffic to attention. The winners won't be those with the most installs — they'll be the ones with the strongest retention and LTV.

We see four things that will separate strong teams from weak ones. Growth in mature categories will come from user switching, not new niches. Retention will fully replace installs as the primary performance metric. A/B testing and Custom Product Pages will become standard practice rather than competitive differentiators. ASO will shift from keyword density to demand management — conversion and intent matching will matter more than the number of keywords in our metadata.

The mobile gaming market in 2026 isn't harder than in 2025. It's just less forgiving of guesswork. If we track the right metrics, test systematically, and understand where our players actually come from, we have a structural advantage over those who don't.

That's exactly why we built the ASOMobile toolkit — keyword research, competitor tracking, conversion analytics, and market intelligence across 90+ countries. The data is there. The question is whether we're using it.

The complete mobile app market report is available here.

Optimize and achieve your goals💙

FAQ: Frequently Asked Questions

According to our data, the combined App Store and Google Play market reached ~$143B in 2025. Games account for 53.9% of Google Play revenue and 46.7% of App Store revenue.

The App Store generates 63.4% of combined revenue while accounting for only 30.3% of downloads. If our goal is monetization, iOS remains the priority platform.

Strategy and Roleplaying lead by revenue on both platforms: on the App Store they generated $9.1B and $8.3B respectively. Casual genres dominate downloads but fall significantly behind in revenue.

Block Blast! proved it works — 368M downloads with zero IAP, purely ad monetization. The key condition is a strong game loop that retains players without financial incentives.

The US remains the largest market by revenue ($15.35B in game revenue on the App Store alone), but competition there is expensive. Turkey is ideal for testing mechanics with low CPI, while Japan offers the highest ARPU in the world.