Welcome to our annual mobile app market report for 2025. In this article, we explore the biggest changes across the App Store and Google Play, category performance, top-ranking apps and mobile games, and the key trends shaping downloads and revenue. We also take a closer look at the evolving competitive landscape and the growing impact of artificial intelligence — and share our outlook on what the mobile app market could look like in 2026.

TL;DR

In 2025, the mobile app market proved once again that growth is no longer driven by explosive install volume, but by stronger monetization, better retention, and AI-powered functionality.

Key Statistics and Facts for 2025

In 2025, the global mobile app market continued to expand, although download growth remained relatively modest.

- Users downloaded 149 billion new apps, up 0.8% year over year.

- In-app purchase (IAP) revenue reached $167 billion, up 10.6% year over year.

- Overall user engagement also increased, with total time spent in mobile apps reaching 5.3 trillion hours (+3.8%).

- On average, users spent 3.6 hours per day in apps and used 34 apps per month.

- On average, each person interacts with about 10 unique apps every day, underscoring the central role mobile services now play in daily life.

The takeaway is clear: users may be installing apps more selectively, but they are spending more time in them — and they are increasingly willing to pay.

Now let’s take a closer look at what 2025 looked like for the mobile app market.

*Please note that this data now includes China

Total iOS & Android Downloads

Growth in mobile app installs has been slowing for several years now, and 2025 was no exception. After the decline in 2024, the market returned to positive growth, but the pace remains moderate.

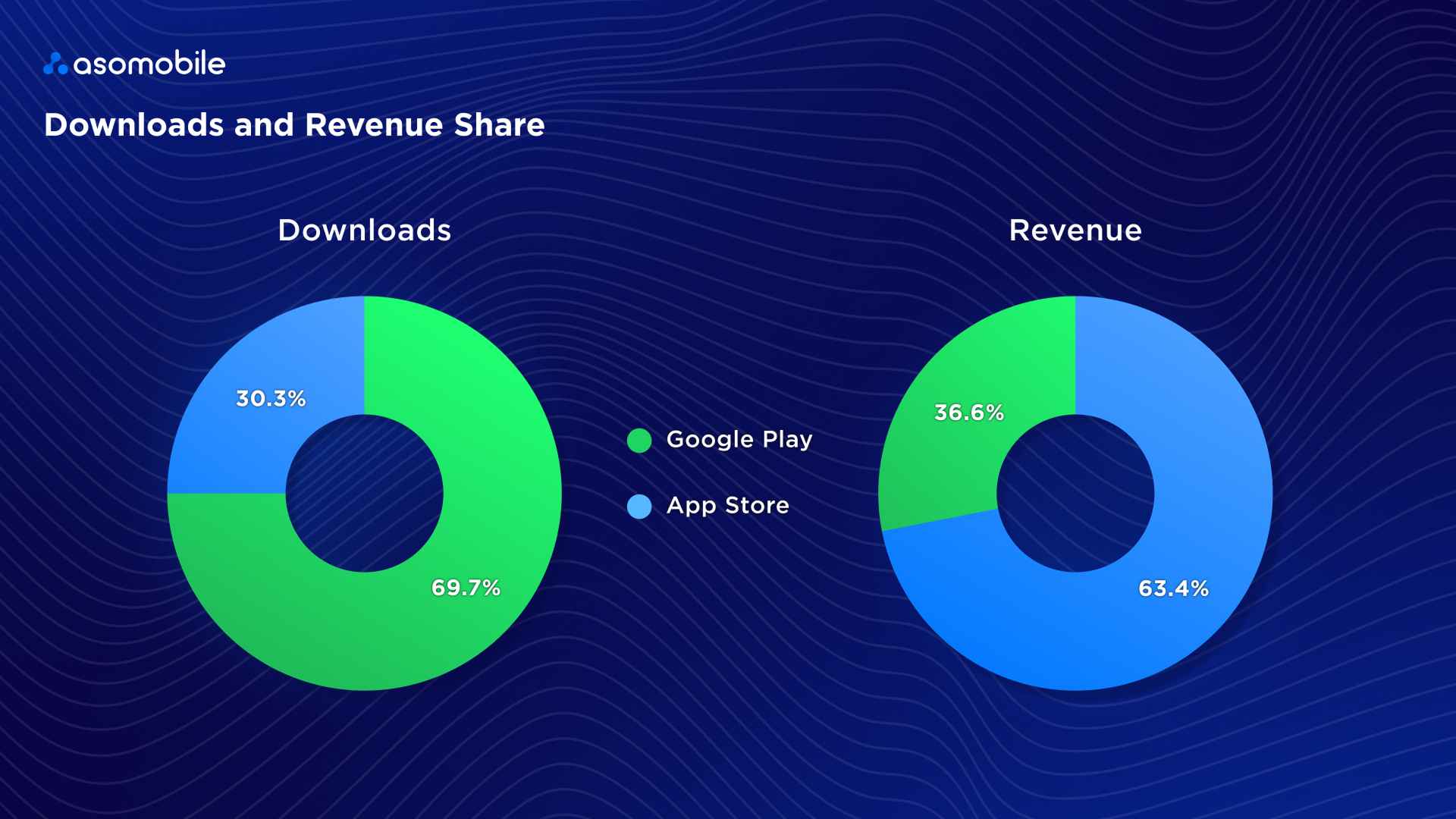

The market is saturated, and users have become more selective. Today, quality matters more than raw install volume. We are closing 2025 with 108.9 billion installs on Google Play and 47.4 billion on the App Store. As usual, Android leads in total game and app installs. That is hardly surprising: Android still dominates the global mobile OS market, accounting for more than 72%.

Top Apps by Downloads in Google Play & App Store

The biggest shift of 2025 was the move of AI apps from hype-driven products into the mainstream. In 2024, ChatGPT ranked only 10th on Google Play (150.1 million downloads) and 4th on the App Store (155.9 million downloads). By 2025, it had become the most downloaded app in both ecosystems, with 766.7 million downloads on Google Play and 222.1 million on the App Store. Another AI app, Google Gemini, also entered the App Store rankings, highlighting how quickly AI services are gaining ground in the mobile space.

Social media and messaging apps remain the foundation of the market, although their positions have shifted slightly. Content platforms and creative tools continue to strengthen their presence. CapCut appears in the rankings across both years and both platforms, while TikTok remains one of the most downloaded apps, confirming the continued popularity of short-form video.

E-commerce and platform services are also gaining ground. Temu was already highly popular in 2024 and maintained strong positions across both platforms in 2025. In the App Store, Google ecosystem services such as Google, Google Maps, and Gmail continue to rank highly, reflecting strong demand for essential everyday tools.

In other words, AI is no longer a niche. It has already become part of everyday mobile demand alongside social media, messaging, and video services.

Now let’s move from downloads to an even more important question: which apps generated the most revenue?

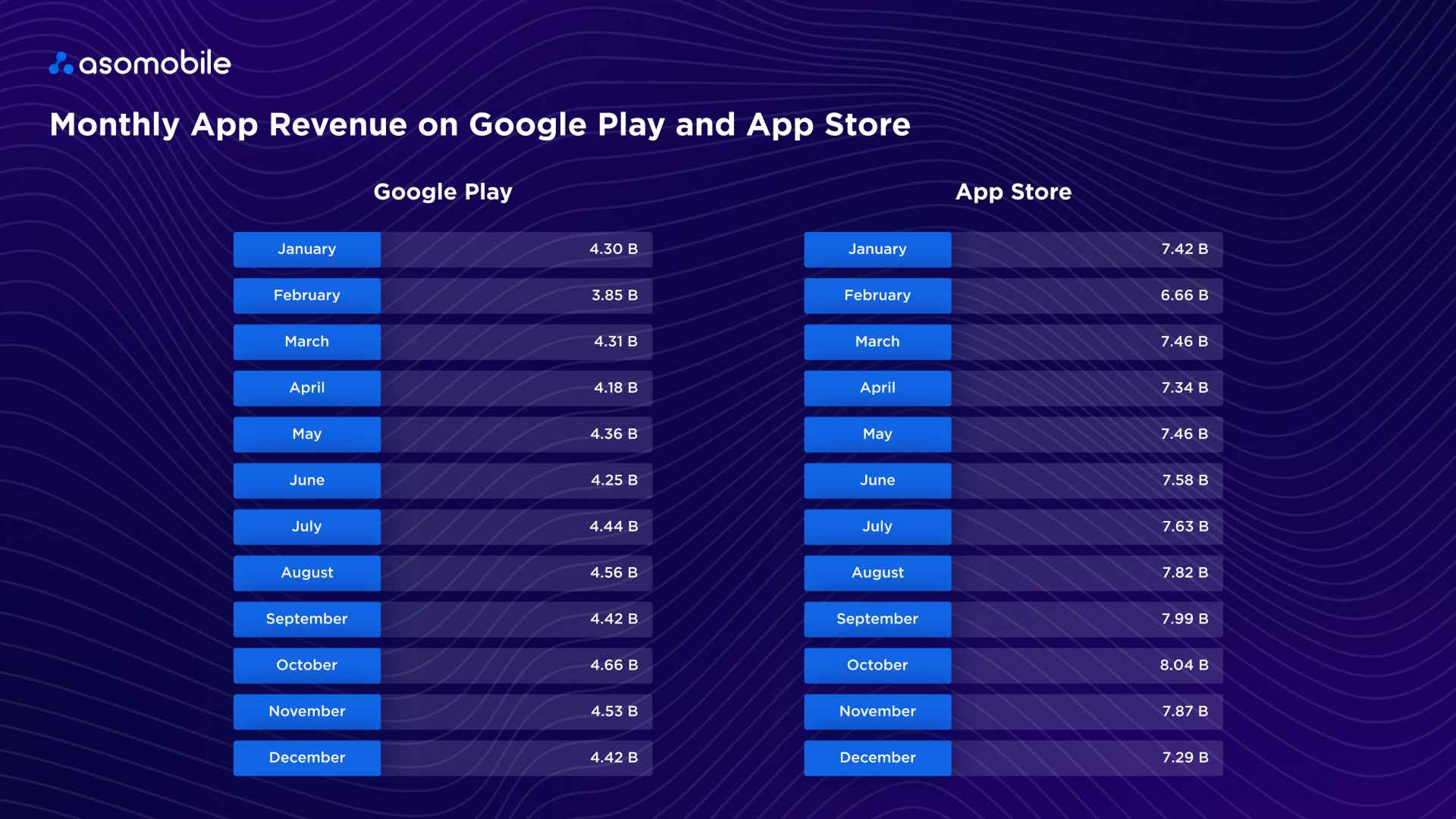

App Revenue in Google Play & App Store

2025 was a strong year for monetization on both platforms, especially within the iOS ecosystem.

Google Play continued to grow, with revenue increasing to $52.3 billion — the highest level across the period covered in this analysis. That means the Android app market added nearly $6 billion in just one year, confirming a gradual recovery in growth after a calmer period between 2021 and 2023.

Apple’s ecosystem is growing much faster in revenue terms. In 2025, App Store revenue rose to $90.6 billion, significantly widening the gap between the two platforms. Part of this growth, however, is due to a methodology update: the Chinese market was included in the 2025 analysis, whereas it had not been counted in previous years.

So which apps drove most of this revenue growth? Let’s look at the top-grossing leaders across both platforms.

In 2025, the ranking structure changed slightly, but the leader remained the same. Google One remained the top-grossing app on Google Play, generating around $2 billion and holding the top spot for the fourth consecutive year.

This is largely driven by the popularity of cloud storage within the Google ecosystem. If you use Android, there is a good chance extra Google One storage is already included in your subscription.

TikTok strengthened its position in second place, reaching approximately $1.2 billion in revenue.

Mobile gaming revenue also surged. Top performers included Last War: Survival Game, Roblox, Royal Match, and MONOPOLY GO!, each approaching the $0.7–0.9 billion range.

The ranking also featured Amazon Shopping, Whiteout Survival, Coin Master, and ChatGPT, reflecting several major market trends at once: growth in e-commerce, mobile gaming, and AI services.

Within the iOS ecosystem, YouTube remained the top-grossing app. It has held the No. 1 spot in revenue since 2020 and remains one of the most stable mobile products in terms of monetization. In 2025, YouTube generated around $4.5 billion.

One of the year’s standout stories was the rapid rise of ChatGPT, which climbed to 2nd place with approximately $3.7 billion in revenue, becoming one of the fastest-growing apps on the platform. TikTok ranked third at around $3.3 billion. The chart also included mobile game leaders such as Last War: Survival Game, MONOPOLY GO!, Royal Match, and Whiteout Survival, as well as the dating app Tinder and subscription platforms like Disney+.

While games and subscription services were the main revenue drivers in 2024, AI apps joined them as major revenue drivers in 2025. This shift is especially visible in the App Store, where many services have seen their revenue increase dramatically. It also reinforces one of the market’s most consistent patterns: iOS users remain more willing to pay, while Android continues to dominate in scale.

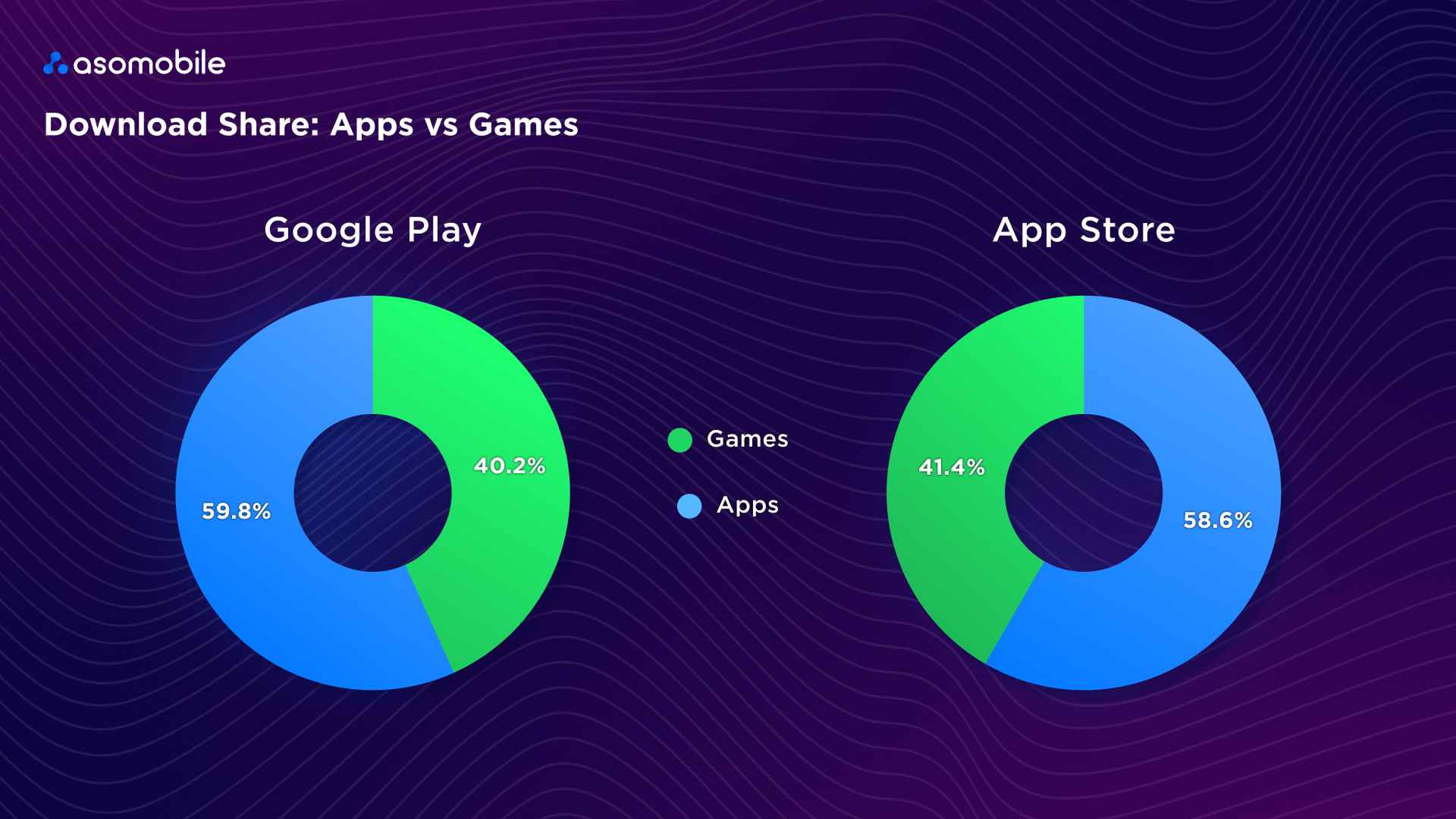

Google Play VS App Store Downloads

The split between downloads and revenue across Google Play and the App Store in 2025 highlights one of the mobile market’s most stable structural realities: Google Play still wins on scale, while the App Store wins on monetization. This asymmetry continues to shape the go-to-market strategy for most developers.

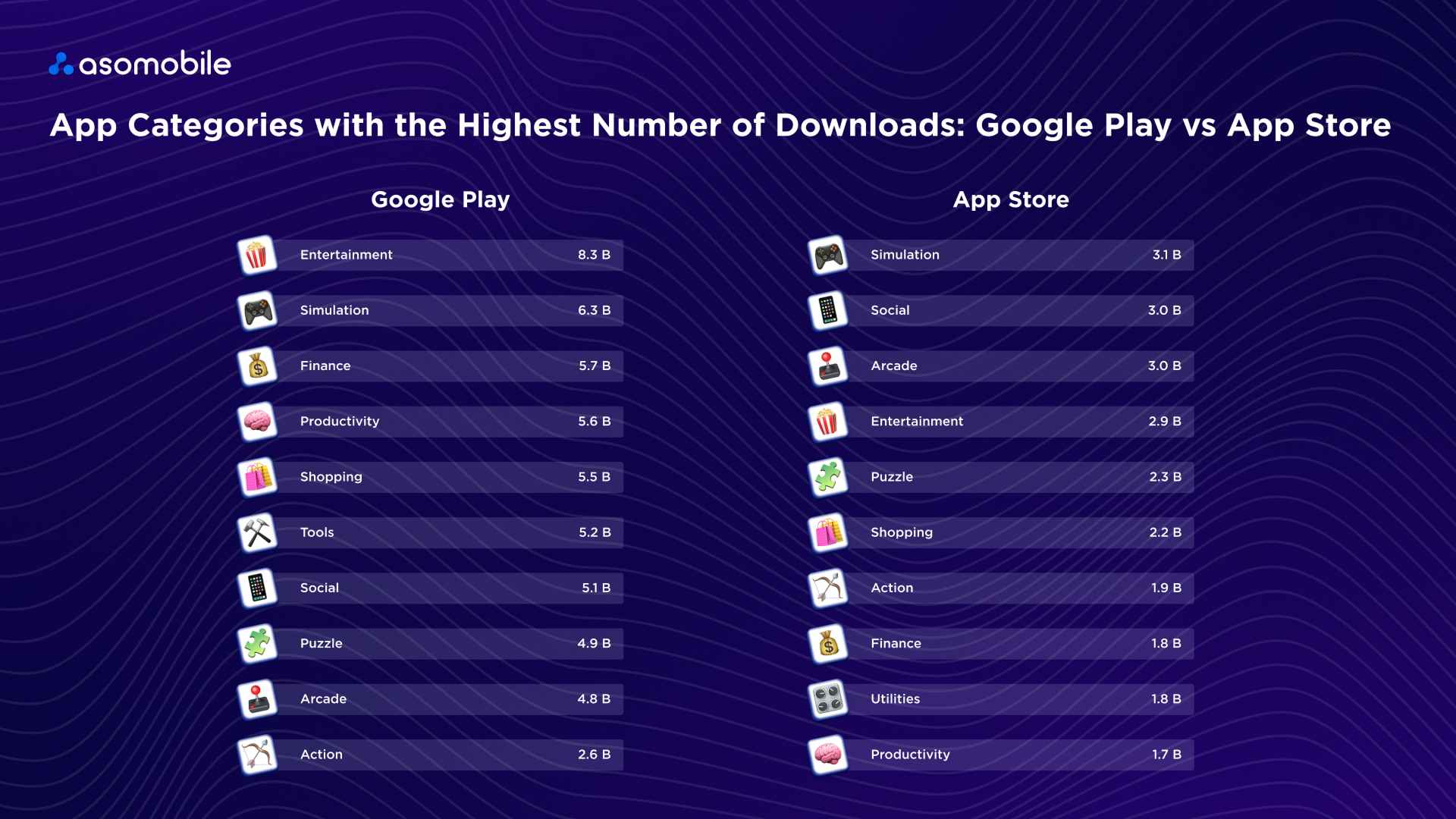

Top Categories by Downloads in Google Play & App Store

In 2025, the overall structure of the most popular app categories remained largely intact, although several notable shifts emerged. On Google Play, entertainment apps and simulation games continued to lead, but compared with 2024, categories such as finance, productivity, and shopping grew much stronger. This reflects the growing importance of mobile banking, work tools, and e-commerce apps in everyday user behavior.

In the App Store, gaming categories also retained leadership — especially simulation games — but arcade, puzzle, and action titles gained a larger share of the top positions. At the same time, social and entertainment apps, along with utility and productivity services, maintained consistently strong performance.

Compared with the previous year, two major trends stand out:

- growth in service-driven categories such as finance, shopping, and utilities,

- continued strength of gaming and entertainment apps, especially within the App Store ecosystem.

This confirms that mobile apps continue to serve two core purposes: entertainment and utility. In 2025, the smartphone fully established itself not just as a screen for leisure, but as a tool for work, payments, and daily life.

So now we know what users install and when. The next question is: how does that translate into revenue? And do users’ installation preferences match their willingness to pay?

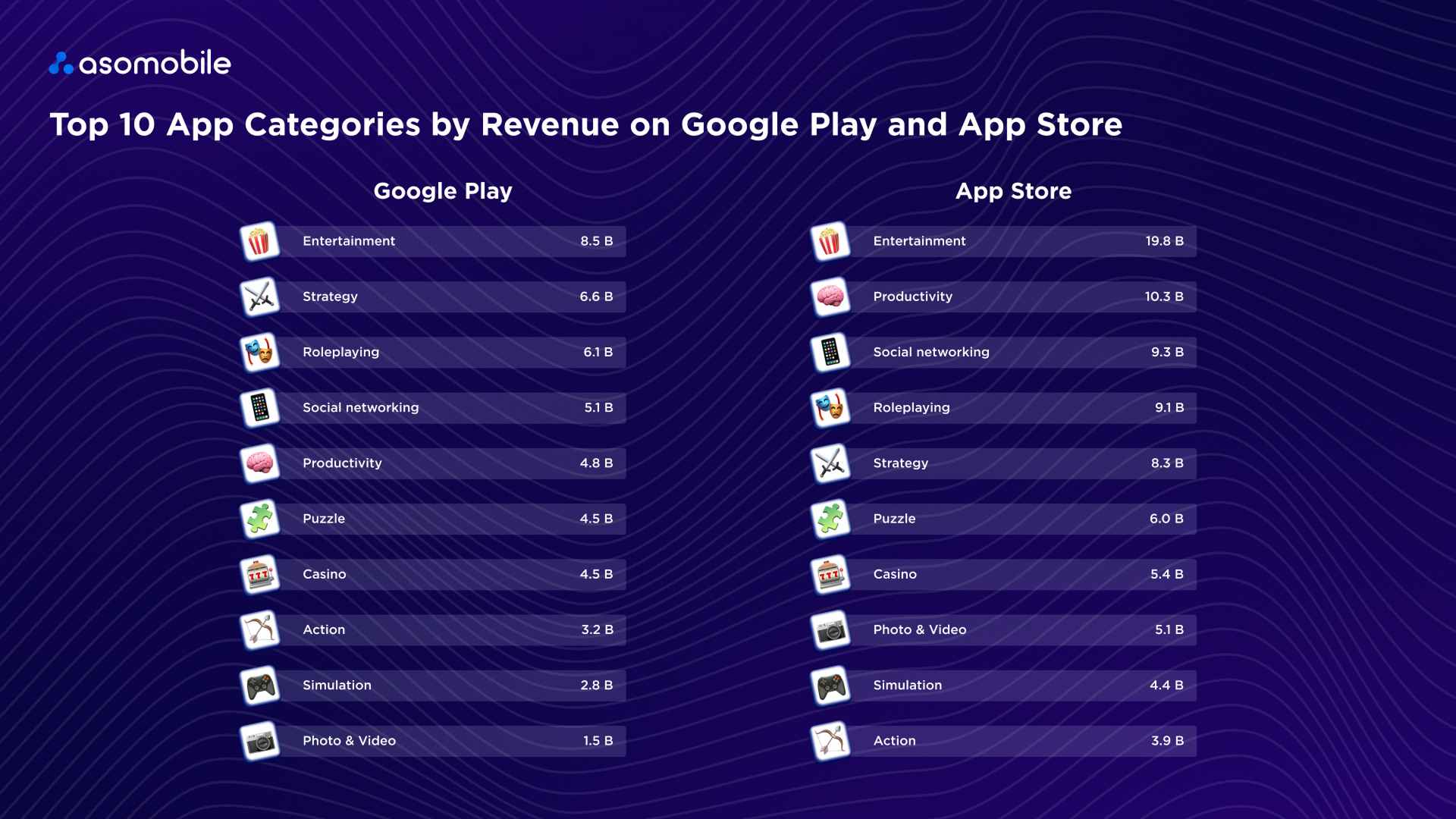

Top Categories by Revenue in Google Play & App Store

The most interesting shift in revenue structure is the visible rise of non-gaming categories. In 2024, the top-grossing categories on both platforms were still dominated by gaming genres such as role-playing and strategy. In 2025, however, Entertainment moved into first place. This reflects stronger revenue from streaming services, media platforms, and subscription-based apps.

That said, gaming categories remain highly important. Strategy, Role-Playing, Puzzle, and Casino continue to rank among the top-grossing categories on both Google Play and the App Store. At the same time, non-gaming categories — especially Productivity and Social Networking — gained significant momentum, driven by rising demand for work tools, communication platforms, and AI-powered services.

On the App Store, growth in Productivity and Social categories is particularly striking, while Google Play shows a more balanced mix of entertainment, gaming, and social apps. Overall, compared with 2024, the market became more diversified in terms of revenue sources: where games once dominated, service and subscription apps now play a much bigger role.

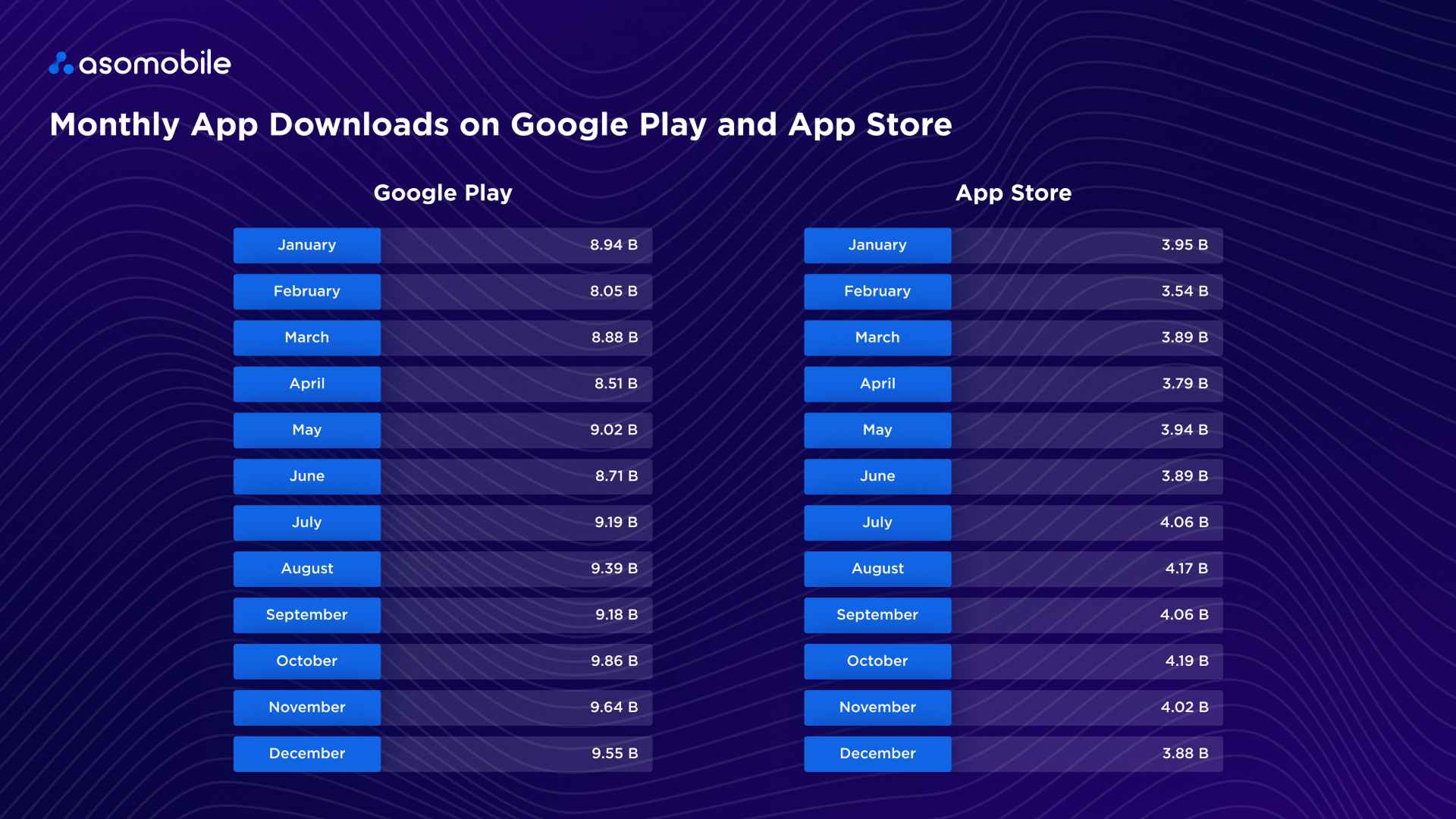

Seasonality of Game and App Downloads

As in the previous year, download activity peaked in the second half of the year — especially in late summer and autumn. Whether it is colder weather, more time spent indoors, or the back-to-school season driving more installs, the pattern is clear. Seasonal download dynamics largely followed the same trend as in 2024, although the overall level of installs was slightly higher. The most active periods still fell between mid-summer and autumn, when downloads gradually increased.

Google Play showed steady growth throughout the year, peaking in late summer and autumn before easing slightly by December. The App Store followed a similar pattern: after a relatively calm start to the year, downloads accelerated in summer and reached their highest levels in early autumn.

Revenue followed a similar seasonal curve — making autumn a golden season not just on the calendar, but for developers too.

Geography of Revenue and Downloads

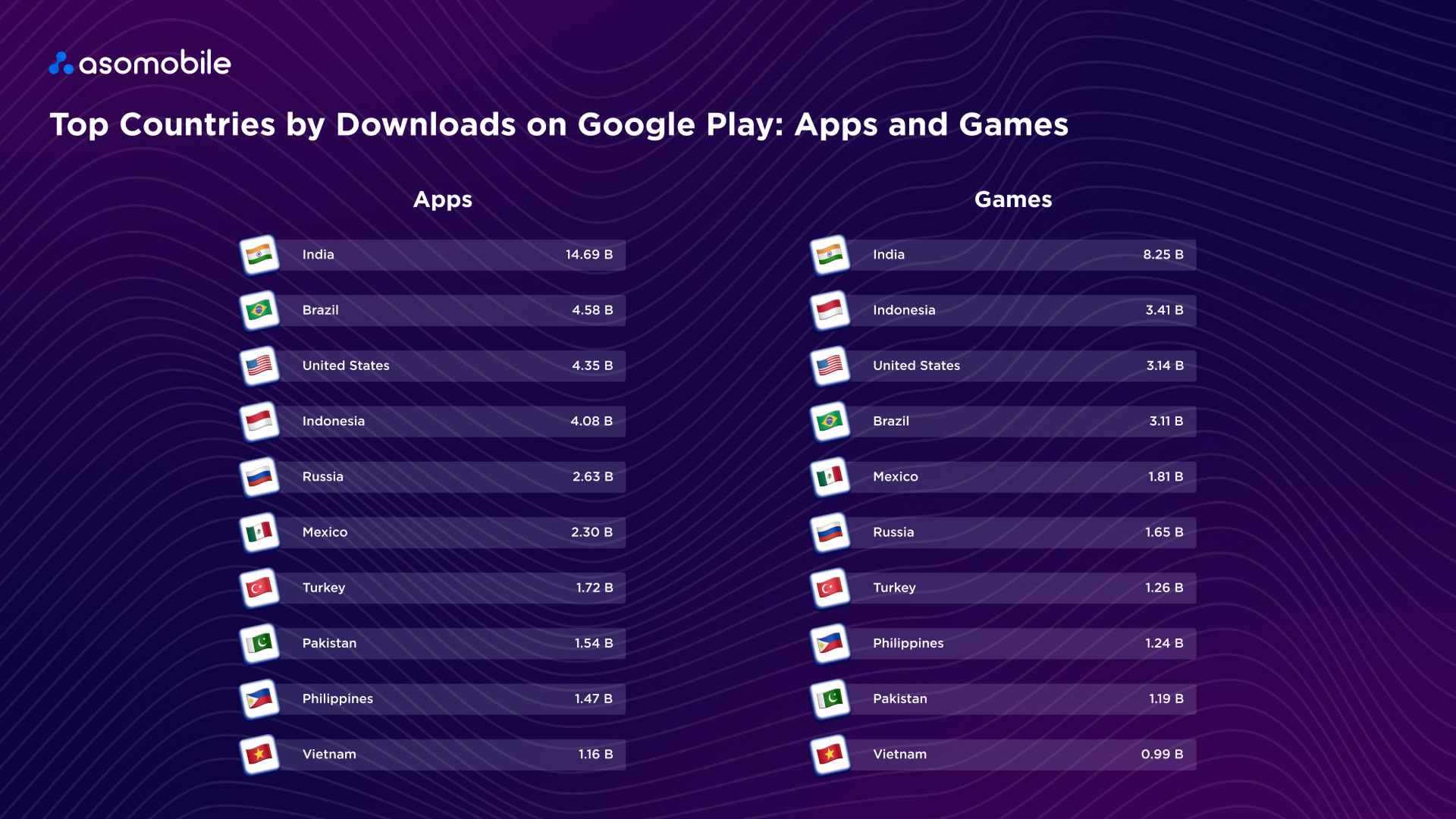

In 2025, the geography of app downloads on Google Play remained broadly similar to the previous year, although there were a few changes within the ranking. India continued to lead by a wide margin, driven by its massive user base and high share of Android devices. It was followed by Brazil, the United States, and Indonesia, which continued to comprise the core group of the world’s largest markets by installed volume.

The picture is similar in mobile gaming: emerging markets continue to drive the largest share of growth. India remained in first place, while Indonesia strengthened its position enough to overtake the United States, reflecting the rapid expansion of gaming audiences across Southeast Asia. Mexico, Turkey, Pakistan, the Philippines, and Vietnam also remained firmly in the global top 10 by downloads.

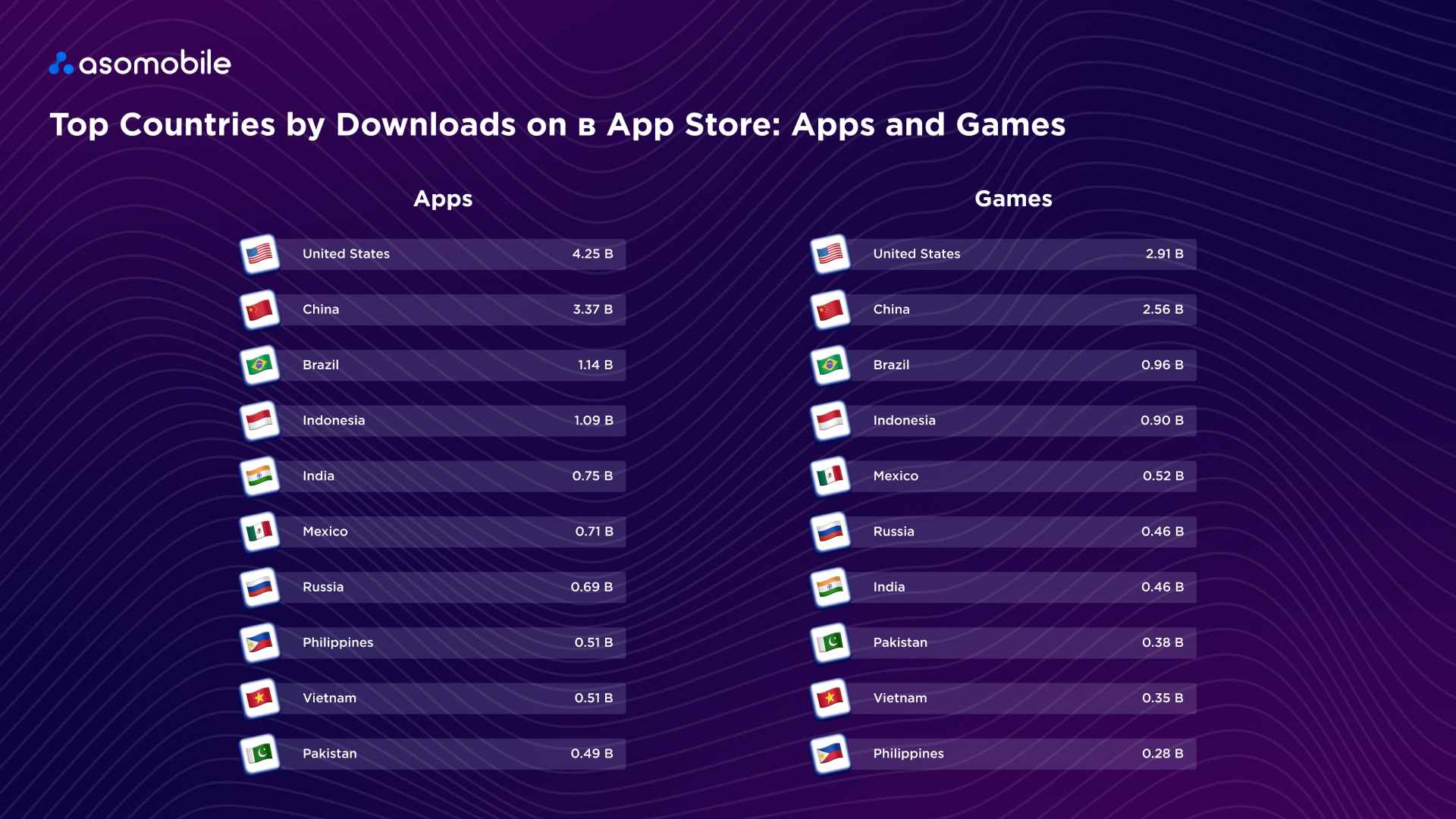

The App Store tells a somewhat different story. Here, more mature markets continue to dominate download rankings.

The United States remained the largest market by install volume for both apps and mobile games, continuing a long-standing trend.

China firmly held second place, strengthening its position significantly versus the previous year. Brazil and Indonesia also remained among the largest App Store markets, consistently ranking near the top.

Interestingly, India — which dominates Google Play — sits much lower in the App Store rankings, closer to the middle of the top 10. This once again highlights the structural differences between the audiences of the two platforms: Android is much more widespread in emerging markets, while iOS remains stronger in countries with a higher concentration of Apple devices.

Overall, the App Store’s top 10 countries by downloads remained relatively stable. No new markets entered the ranking, and most changes were limited to minor shifts within the top 10.

However, once we move from installs to revenue, the picture changes much more dramatically — and the revenue geography of the mobile market looks very different.

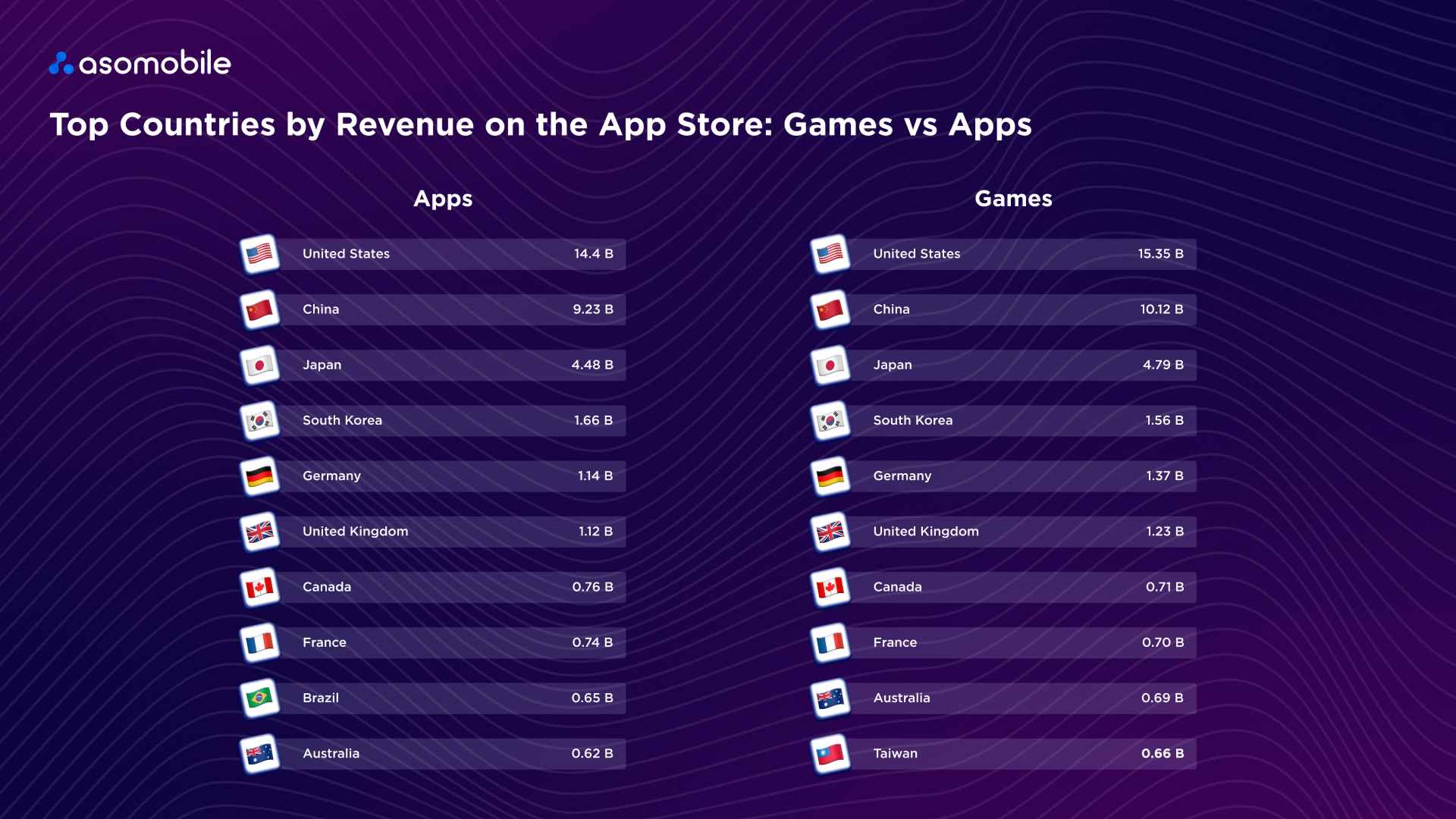

Revenue by Country in Google Play & App Store

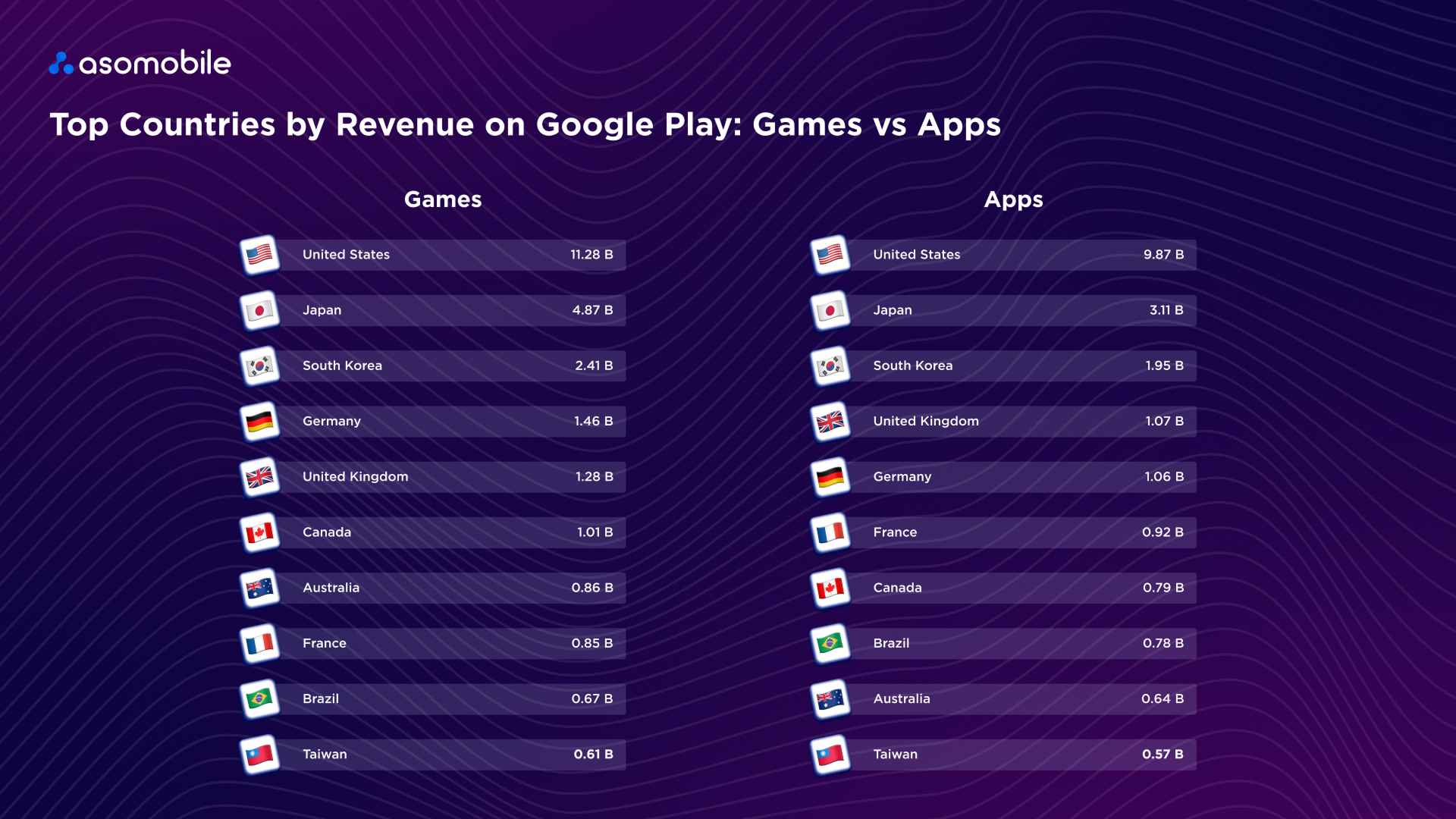

Google Play revenue distribution looks very different from its download distribution. Revenue remains concentrated in more developed, higher-spending markets.

The United States remains the clear leader in both apps and mobile games, with a significant gap over every other country.

Japan continues to rank second, having long remained one of the world’s largest and most profitable mobile gaming markets. South Korea follows close behind, known for its highly engaged audience and strong willingness to pay for mobile content.

European markets such as the United Kingdom, Germany, and France also continue to rank highly.

Interestingly, markets with the highest download volumes are not always the biggest revenue generators. Countries such as India and Indonesia, for example, contribute a major share of global installs but remain much less prominent in revenue rankings.

By contrast, countries with higher user purchasing power — such as Canada, Australia, and Taiwan — appear regularly in the top 10.

Overall, Google Play’s top 10 revenue markets remain relatively stable: new entrants appear rarely, and most changes come from minor reshuffling within the ranking.

The App Store revenue picture is broadly similar — but even more pronounced.

The United States remains the undisputed leader in App Store revenue across both apps and mobile games. As the world’s largest iOS market, it unsurprisingly accounts for a major share of global revenue.

China firmly holds second place and shows particularly strong performance in mobile gaming. Japan remains third, one of the most consistent and lucrative mobile gaming markets in the world.

South Korea, Germany, and the United Kingdom follow closely behind, having remained key revenue markets for developers for many years.

Canada, France, and Australia also appear regularly in the top 10, supported by high user purchasing power and well-established in-app spending habits.

Brazil is another interesting example: despite its high install numbers, it still trails significantly behind more mature markets in revenue terms.

Overall, the App Store revenue ranking remains quite stable. The biggest players continue to hold their positions, and most changes happen through small internal reshuffles rather than the arrival of new markets.

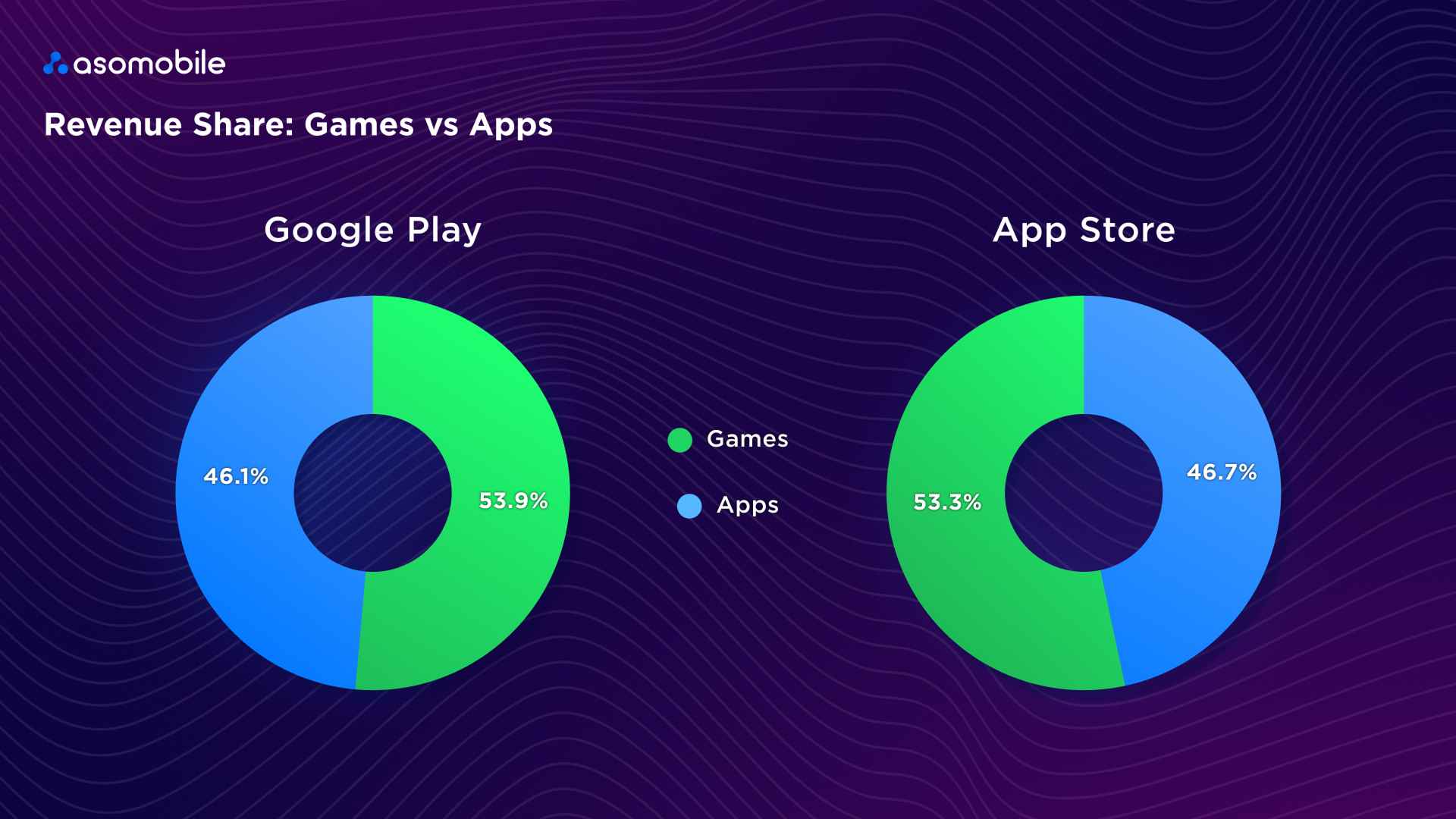

Apps VS Games — Downloads and Revenue

Apps continue to lead in total installs because they cover users’ everyday needs and routines.

Games, however, continue to dominate revenue because the gaming industry remains the most effective at monetizing engagement.

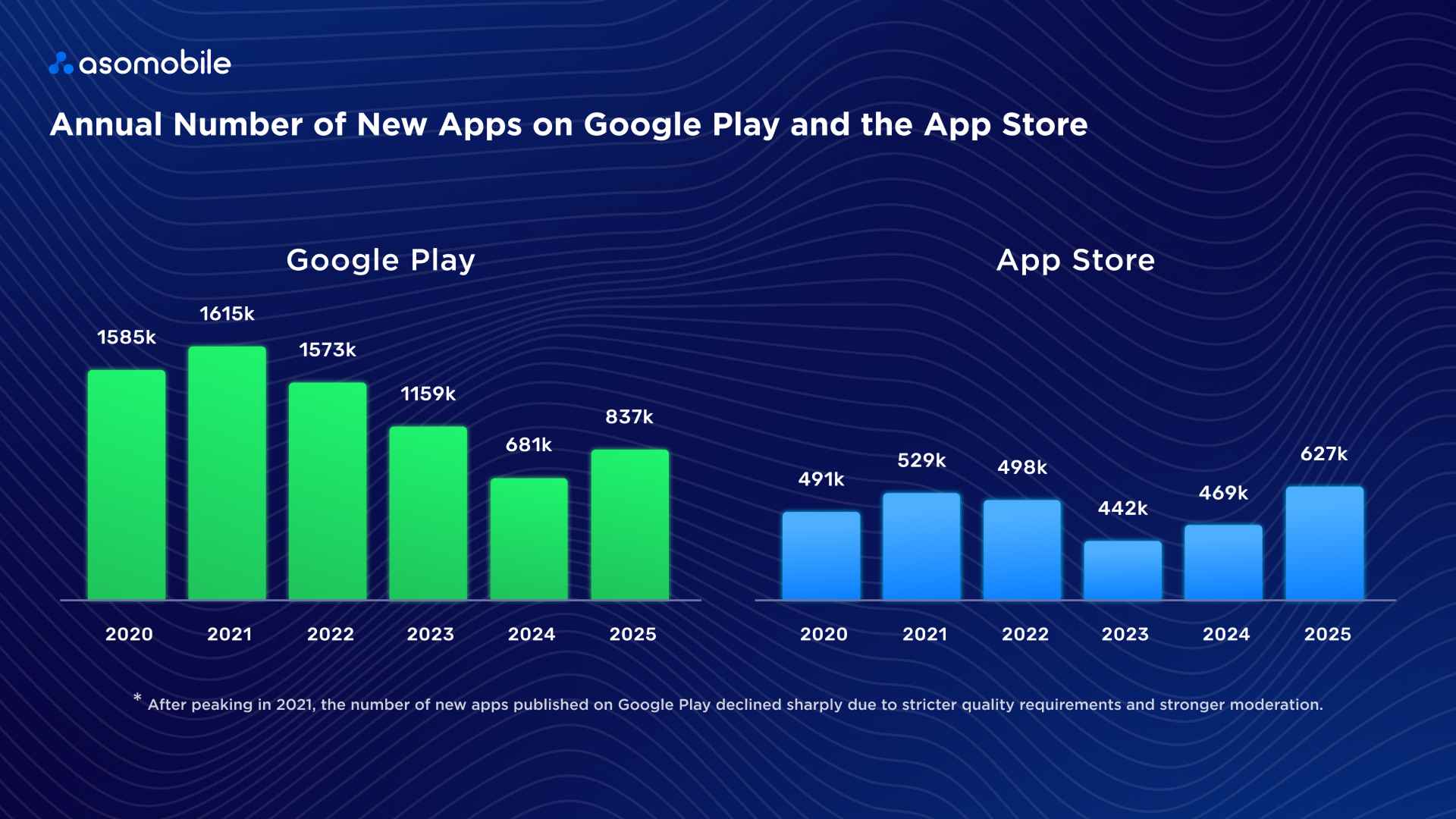

New Apps

If we look at the pace of new app releases, it is clear that after peaking in 2021, the market went through a period of significant cleanup. On Google Play, the number of new releases dropped from more than 1.6 million in 2021 to around 680,000 in 2024. This was largely driven by stricter app-quality requirements and tighter moderation by Google.

In 2025, the market began to recover gradually, with the number of new apps on Google Play rising to approximately 837 thousand.

The App Store showed a steadier pattern. After a slight decline in 2023, the number of new releases began to increase again, rising from 469 thousand in 2024 to around 627 thousand in 2025.

Even so, the market still offers strong potential for new breakout hits: despite tighter moderation and fierce competition, a strong product can still grow rapidly from newcomer to category leader.

2025 Results and Forecasts for 2026

How 2025 Ended

Despite moderate install growth and a more cautious pace of new app launches, the mobile market continued to grow. The main driver of that growth was not install volume, but monetization efficiency.

Developers are increasingly focusing on their existing user base by expanding subscription models, in-game purchases, and personalized offers.

In many ways, the market has now fully entered a maturity phase: app success depends less on how many installs it can generate and more on retention and long-term user value.

Growth of Subscriptions and In-Game Purchases

In 2025, the subscription model firmly established itself as one of the core monetization tools for both service apps and mobile games.

Users are increasingly willing to pay for convenience, ongoing access to content, and additional features. That is why the freemium model remains the most resilient: free access helps scale the audience, while subscriptions and premium features create stable recurring revenue.

What this means for developers

User LTV is becoming a more important success metric than one-time purchases.

Subscriptions only work well when engagement is high, so improving the user experience must remain a constant priority. Overly aggressive monetization, on the other hand, can drive churn.

To improve subscription performance, developers should:

- use AI algorithms to personalize offers,

- optimize the path to subscription,

- make payments as seamless as possible through Apple Pay and Google Pay.

The Growing Popularity of Non-Gaming Apps

Non-gaming apps continue to strengthen their position in download rankings. Users are increasingly choosing multifunctional services that combine communication, content creation, AI tools, and everyday automation into a single experience.

What this means for developers

Competition within categories is becoming more intense than ever. As a result, a unique user experience is increasingly becoming the key growth differentiator.

At the same time, retention is gradually becoming more important than acquisition. Many services are now focused on building long-term relationships with users rather than relying on short-term bursts of installs.

In 2025, the most successful apps are actively investing in:

- AI-powered personalization of interface and content,

- cross-platform ecosystems (mobile + web),

- integrations with other services to drive deeper engagement

Slower Install Growth

Download growth continues to slow — another clear sign of a mature market. Acquiring new users is getting more expensive, and cost per install (CPI) is gradually rising.

What this means for developers

Retention is becoming one of the most important success metrics.

UX, engagement, and overall product experience now directly impact app revenue. More and more often, monetization is built around active users rather than total installs.

To offset slowing download growth, developers are doubling down on:

- personalized user experiences,

- re-engagement mechanics,

- hybrid monetization models (subscriptions + in-app purchases).

AI Apps as a New Market Driver

The AI app segment became one of the fastest-growing categories in 2025. Generative AI is no longer just a standalone product — it is increasingly being embedded into service apps across the board.

AI is gradually shifting from a technology trend to a must-have element of product competitiveness.

What this means for developers

AI services require significant computing power and infrastructure, while users expect high accuracy and output quality.

That is why monetization for these products is most often built around freemium models and subscriptions.

Companies are actively investing in:

- embedding AI features directly into apps,

- personalizing content and recommendations,

- AI tools are designed to improve retention.

Key Market Takeaways

Revenue leaders. Games remain the largest revenue category, but service apps are gradually closing the gap through subscriptions and paid content.

Market globalization. Emerging markets continue to generate the majority of downloads, while revenue remains concentrated in the United States, Japan, and South Korea.

iOS vs Android downloads. Android continues to lead in total installs, while iOS users remain the more valuable paying audience.

Popular categories. Entertainment services, short-form video, and communication platforms continue to show the strongest momentum.

Apps vs games. Apps lead in installs, but mobile games remain the market's core revenue driver.

New apps. The volume of new releases stabilized after stricter moderation, but competition in the stores continues to intensify.

Forecasts for 2026

In 2026, competition in the mobile market will be driven less by traffic and more by user attention.

The main shifts likely to shape the market include:

1. Stronger competition in mature categories. Growth will come less from new niches and more from audience redistribution across existing services.

2. Retention will become the key metric. User retention is steadily replacing installs as the primary growth KPI.

3. AI will become the main personalization engine. Generative AI will increasingly be used for content creation, recommendations, and user experience optimization.

4. Short-form video will continue to drive app growth. Short-video and short-drama formats will remain important drivers of engagement.

5. Marketing will shift from traffic to engagement. Companies will continue investing more heavily in retention and ecosystem development around their products.

6. Development will accelerate thanks to AI tools. AI will help teams test hypotheses faster and ship new features more efficiently.

The mobile market is still growing, but the rules are changing. Where app success once depended on install scale, it now increasingly depends on retention, personalization, and long-term product value.